India has entered the new financial year 2026, bringing several rule changes that directly impact salaries, taxes, and daily financial transactions. From revised TDS norms to updated ATM and FASTag rules, these changes will influence how individuals and businesses manage money.

New Financial Year 2026: What Has Changed for Taxpayers

The new financial year 2026 introduces multiple compliance and tax-related updates aimed at improving transparency and digital tracking. Key changes include revised Tax Deducted at Source thresholds and stricter reporting requirements for high-value transactions.

For salaried individuals, employers are expected to align payroll systems with updated tax structures from April 1. This affects in-hand salary calculations, especially for those opting between old and new tax regimes. The new regime continues to gain traction due to simplified slabs, although exemptions remain limited.

Additionally, taxpayers will see changes in how financial institutions report transactions. Higher scrutiny on large deposits and withdrawals is expected, which may impact individuals operating in cash-heavy environments, particularly in Tier-2 and Tier-3 cities.

Salary Impact and Payroll Adjustments in FY26

Salary structures in FY26 are being recalibrated to align with compliance requirements and cost optimisation strategies. Many companies are restructuring components such as allowances and reimbursements to fit within updated tax frameworks.

Provident Fund contributions and gratuity calculations remain largely unchanged, but the tax treatment of certain allowances may differ depending on the chosen tax regime. This makes salary planning more important than before.

For employees, the key shift is the growing preference for the new tax regime. It offers lower tax rates but removes many deductions. As a result, individuals who previously relied on tax-saving investments will need to reassess their financial planning strategies.

ATM, FASTag and Digital Transaction Rules Updated

Several changes in daily transactions have come into effect with the start of the financial year. ATM withdrawal rules have been updated, with some banks revising free transaction limits and charges after exceeding thresholds.

FASTag regulations have also been tightened to ensure seamless toll payments and reduce fraud. Non-compliant FASTags may face deactivation, affecting highway travel for frequent commuters and logistics businesses.

Digital payments continue to see policy focus. The government and regulators are pushing for stronger authentication systems and improved fraud monitoring. This is particularly relevant for small businesses and shop owners who rely heavily on UPI and card payments.

Impact on Small Businesses and Tier-2 Economies

The new financial year changes are especially significant for small businesses and traders in non-metro regions. Increased compliance requirements and transaction tracking mean businesses need better record-keeping and digital adoption.

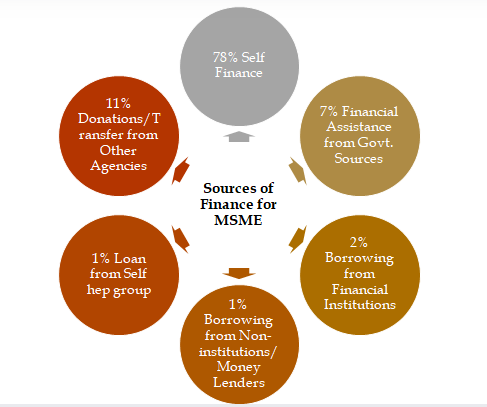

For MSMEs, access to credit may improve due to better financial data visibility. However, stricter reporting norms could initially create operational challenges for businesses transitioning from informal to formal systems.

Local traders, transport operators, and service providers will also feel the impact of FASTag and digital payment regulations. Over time, these changes are expected to improve efficiency and reduce leakages in the system.

Government Strategy Behind FY26 Financial Changes

The broader objective behind these changes is to formalise the economy and strengthen tax compliance. By tightening reporting systems and encouraging digital transactions, the government aims to widen the tax base without increasing tax rates.

The continued push towards the new tax regime indicates a long-term shift towards simplified taxation. At the same time, transaction-level monitoring helps authorities track economic activity more accurately.

These changes also align with India’s digital economy goals, where transparency and traceability play a central role in financial governance.

Takeaways

- New financial year 2026 introduces updated tax and transaction rules affecting individuals and businesses

- Salaried employees may see changes in in-hand income due to revised payroll structures

- ATM, FASTag, and digital payment rules are becoming stricter to improve compliance

- Small businesses in Tier-2 and Tier-3 regions need to adapt to increased financial tracking

FAQs

What is the biggest change in FY26 for taxpayers?

The increased focus on the new tax regime and stricter reporting of financial transactions are the most significant changes.

Will my salary decrease due to new rules?

Not necessarily. However, changes in tax calculations and allowances may slightly alter your take-home salary.

Are ATM withdrawal rules different now?

Yes, some banks have revised free transaction limits and charges beyond those limits.

How do these changes affect small businesses?

Small businesses will need better compliance and digital systems, but they may benefit from improved access to credit.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Leave a comment