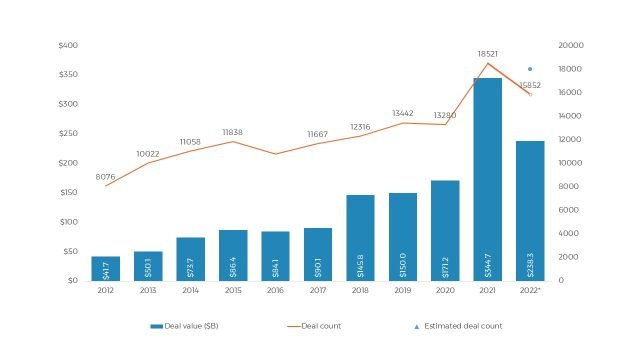

Post-2025 funding winter has reshaped how venture capital flows into Indian startups, forcing investors to become selective and founders to adapt quickly. As 2026 begins, capital is returning with caution, clarity, and sharper expectations around governance, profitability, and execution quality.

Post-2025 funding winter is a time sensitive topic with forward looking relevance. The tone remains analytical and news oriented, reflecting how venture capital behavior is evolving right now rather than offering abstract theory.

How the Post-2025 Funding Winter Changed Venture Capital Behavior

Post-2025 funding winter marked the end of easy capital and momentum driven investing. Venture capital firms slowed deployment, reduced fund sizes, and extended decision cycles. Many funds shifted focus from sourcing new deals to supporting existing portfolio companies through runway extensions and cost discipline.

The correction forced VCs to reassess risk models. Growth projections without margin visibility lost credibility. Capital efficiency, governance, and founder execution became non negotiable. This reset was not limited to India but felt sharper due to the aggressive funding cycles of earlier years.

Secondary keywords like venture capital discipline and startup funding slowdown explain why deal volumes dropped even as dry powder remained available.

VC Selectivity Becomes the Dominant Theme in 2026

VC selectivity defines the early 2026 outlook. Investors are not chasing deal flow. They are filtering aggressively. Fewer startups make it past initial screening, and those that do face deeper diligence.

Founders are expected to demonstrate revenue quality, customer retention, and realistic expansion plans. Story driven pitches no longer suffice. Sector expertise and operational clarity matter more than brand buzz.

This selectivity also shows in cheque sizes. Many funds prefer smaller initial investments with clear follow on triggers. Secondary keywords such as selective venture capital and milestone based funding capture this shift.

Sector Wise Recovery Patterns in Venture Capital Flow

Not all sectors recover equally after the post-2025 funding winter. Infrastructure fintech, SaaS, climate tech, deeptech, and B2B platforms show early signs of capital inflow. These sectors offer predictable revenue, longer contracts, or policy aligned demand.

Consumer internet and quick commerce remain under pressure due to margin challenges and high competition. Fintech lending and BNPL models face scrutiny over asset quality and regulatory exposure.

Healthcare, manufacturing tech, and logistics solutions tied to MSMEs attract selective interest, especially when unit economics are proven. Sector wise VC recovery will remain uneven through 2026.

Early Stage Versus Late Stage Capital Dynamics

Post-2025 funding winter affected late stage capital more severely than early stage funding. In 2026, early stage deals continue, though with stricter founder evaluation and slower closure timelines.

Late stage investments are highly selective and often structured. Down rounds, flat rounds, and secondary transactions are common. IPO readiness and profitability timelines dominate discussions.

Secondary keywords like early stage venture funding and late stage startup valuation trends help explain why capital flows differ by stage rather than disappearing entirely.

Role of Domestic Capital and New Investor Profiles

One notable change after the post-2025 funding winter is the rising role of domestic capital. Indian family offices, corporate venture arms, and sector focused funds are more active in 2026.

These investors prefer businesses aligned with long term national growth themes rather than rapid global expansion. Their investment horizons are often longer, with less pressure for quick exits.

Foreign investors remain present but cautious. They focus on governance, compliance, and exit visibility. This mix creates a more balanced capital base compared to earlier cycles.

Founder Strategy Adjustments to Match VC Expectations

Founders have adapted quickly to post-2025 funding winter realities. Many startups reduced burn, exited non core markets, and refocused on profitable segments. Hiring slowed, but senior leadership quality improved.

Fundraising strategies now involve longer preparation, clearer metrics, and realistic valuation expectations. Founders pitch fewer investors but with deeper engagement.

This strategic maturity improves startup survival rates and aligns businesses with what VCs want to back in 2026.

What a Recovery Really Looks Like in 2026

The recovery after the post-2025 funding winter is not a return to excess. It is a recalibration. Capital flows are steadier, more thoughtful, and tied to execution outcomes.

Deal volumes may rise gradually, but mega rounds will remain rare. Exits through M&A, secondary sales, and selective IPOs will matter more than unicorn counts.

This recovery rewards discipline over hype and resilience over speed.

Long Term Implications for the Venture Capital Ecosystem

Over the long term, the post-2025 funding winter strengthens the ecosystem. Weak models fail early. Strong founders gain leverage. Investors improve returns by backing fewer but better companies.

The relationship between founders and investors becomes more transparent and collaborative. Capital allocation improves, and systemic risk reduces.

While the pace of innovation may slow temporarily, the quality and durability of outcomes improve.

Takeaways

- Post-2025 funding winter has permanently increased VC selectivity

- 2026 recovery favors capital efficient and governance ready startups

- Sector wise and stage wise recovery remains uneven

- Domestic capital plays a larger role in venture funding flows

FAQs

Is venture capital funding recovering in 2026?

Yes, but selectively. Capital is returning to strong startups with clear fundamentals rather than broadly across the market.

Which startups benefit most after the funding winter?

Startups with proven unit economics, predictable revenue, and disciplined founders benefit the most.

Are valuations improving again in 2026?

Valuations are stabilising, not inflating. Investors remain cautious and valuation sensitive.

Will funding winters repeat in the future?

Yes. Funding cycles are structural. The difference now is that both founders and investors are better prepared.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Leave a comment