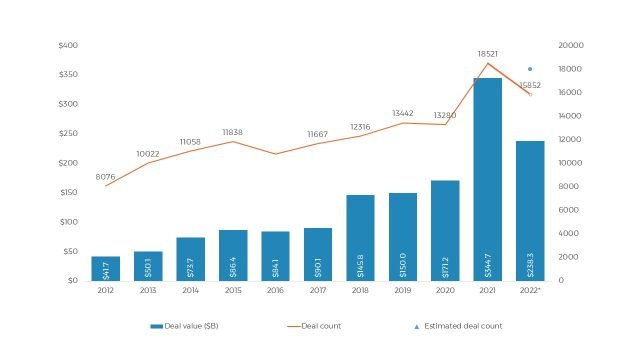

VC selectivity deepens as investors write fewer checks but bigger tickets, reshaping how capital flows through India’s startup ecosystem. The shift in allocation behavior reflects caution, portfolio consolidation, and a clear preference for scale ready companies with proven execution.

VC selectivity deepens across India’s venture capital landscape as investors reduce the number of deals they close while increasing the size of individual investments. This change marks a structural evolution rather than a temporary slowdown. Capital is still available, but it is being deployed differently, with sharper filters, longer conviction cycles, and a stronger focus on outcomes.

Fewer deals reflect higher investment thresholds

The decline in deal count is a direct outcome of stricter evaluation standards. Venture capital firms are no longer spreading capital across dozens of early and mid stage bets. Instead, they are applying higher thresholds on traction, revenue visibility, and governance before committing funds.

This approach reduces exposure to uncertainty. Investors prefer backing companies that have already crossed key risk milestones rather than funding experimentation. As a result, startups that once could raise capital on potential alone now face extended fundraising timelines or rejections.

The emphasis has shifted from idea validation to execution validation. Fewer checks does not indicate lack of interest. It signals a recalibration of what qualifies as investable.

Bigger tickets driven by portfolio concentration

While deal counts have fallen, ticket sizes have grown for companies that clear investor filters. This reflects portfolio concentration strategies. Funds are allocating more capital to fewer startups where conviction is highest.

Larger tickets allow investors to protect earlier positions, support scale, and influence outcomes more directly. Follow on rounds now account for a greater share of deployed capital compared to new investments.

This concentration reduces dilution risk for strong performers and aligns investor incentives with long term value creation. It also reflects limited appetite for spreading capital thinly across uncertain bets.

Capital allocation shifts toward late stage strength

VC allocation behavior in 2025 and beyond increasingly favors late stage and growth stage companies. These startups offer clearer visibility on revenue, margins, and exit potential. Investors see them as lower risk in volatile macro conditions.

Early stage investing has not stopped, but it has slowed relative to late stage deployment. When early stage deals do happen, they often involve experienced founders or niche enterprise focused models.

This shift impacts the capital ladder. Startups that survive early stages face intense competition for growth capital, while those that reach scale are rewarded with larger, more decisive rounds.

Sector preferences reinforce selectivity

Sector preferences play a major role in this allocation shift. Investors are concentrating capital in sectors where business models align with public market expectations and long term demand.

Enterprise technology, fintech infrastructure, and B2B platforms benefit from this trend. These sectors offer predictable revenues, longer customer relationships, and compliance friendly narratives. Consumer focused and capital intensive models face higher scrutiny unless profitability is visible.

By writing bigger tickets in fewer sectors, investors reduce complexity and improve benchmarking across portfolios. This reinforces selectivity at both the company and sector level.

Impact on founders and fundraising strategy

For founders, deepening VC selectivity changes how fundraising must be approached. Pitch narratives focused on vision alone are insufficient. Investors expect clarity on unit economics, customer acquisition efficiency, and operational discipline.

Fundraising cycles have lengthened. Founders are raising capital less frequently but in more substantial rounds once milestones are achieved. This reduces distraction and aligns capital deployment with execution phases.

However, the bar to access capital has risen. Founders without strong metrics or differentiation face limited options, forcing many to bootstrap longer or explore alternative funding sources.

Why investors prefer fewer, larger bets

Writing fewer checks but bigger tickets allows investors to manage portfolios more actively. Board involvement, strategic guidance, and operational support become more feasible when portfolios are smaller.

This approach also aligns with exit realities. With IPOs and acquisitions becoming more selective, investors want to back companies that can realistically reach liquidity events. Larger tickets into proven companies increase the probability of meaningful exits.

Risk management is central to this strategy. Instead of diversifying through volume, investors diversify through depth and conviction.

Consequences for the startup ecosystem

The ecosystem impact of VC selectivity is mixed. On one hand, it filters out weak business models early, improving overall quality. On the other, it reduces experimentation and limits access to capital for unconventional ideas.

Early stage founders feel the pressure most. Angel investors and micro funds partially fill the gap, but institutional capital enters later than before. This elongates the startup journey.

Over time, this could lead to fewer startups but stronger survivors. The ecosystem becomes leaner, more disciplined, and more aligned with sustainable growth.

What this trend signals going forward

The shift in VC allocation behavior is likely to persist. Macroeconomic uncertainty, public market discipline, and limited exit windows reinforce selectivity.

Future capital deployment will reward founders who understand this reality and build accordingly. Metrics, governance, and execution will matter more than momentum.

VC selectivity deepens not because capital has vanished, but because expectations have matured. The ecosystem is adjusting to a more durable investment model.

Takeaways

VCs are writing fewer checks as investment thresholds rise across stages

Bigger tickets reflect portfolio concentration and higher conviction

Late stage and enterprise focused startups benefit most from this shift

Founders must prioritise execution, metrics, and governance to raise capital

FAQs

Why are VCs writing fewer checks now?

Investors are applying stricter filters to reduce risk and focus on proven execution rather than broad experimentation.

Why are ticket sizes increasing despite fewer deals?

Funds are concentrating capital into fewer startups where conviction is strongest, often through follow on rounds.

Which startups benefit most from this trend?

Late stage, enterprise tech, and fintech infrastructure startups with predictable revenues benefit the most.

Is early stage funding disappearing?

No, but it is becoming more selective and founder quality driven, with smaller pools of institutional capital.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Leave a comment