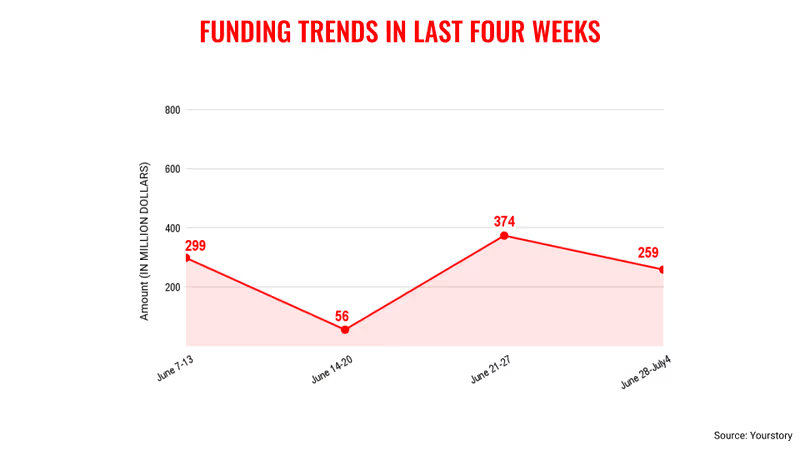

Indian startups raised $200 million across 31 deals this week, reflecting steady investor interest despite a selective funding environment. The weekly funding snapshot shows capital flowing into early stage and growth stage ventures, with fintech, SaaS and consumer brands leading activity.

Indian startups raised $200 million across 31 deals this week, according to the latest weekly funding snapshot tracking venture capital and private equity investments. While the total value is modest compared to peak funding years, the distribution of deals indicates sustained momentum in early stage innovation and disciplined growth capital deployment.

The current funding cycle reflects a shift from aggressive capital deployment to measured, sector specific investments. Investors are prioritizing sustainable business models, clear revenue visibility and realistic valuations. The spread of 31 deals suggests that capital is being allocated across multiple sectors rather than concentrated in a few large transactions.

Deal Volume Signals Early Stage Confidence

A significant portion of the 31 deals involved seed and Series A rounds. This trend indicates that venture capital firms continue to back new founders despite global macroeconomic uncertainties. Early stage investing typically focuses on technology platforms, digital services and emerging consumer brands.

Smaller ticket sizes reduce downside risk while preserving upside potential. For founders, this environment encourages capital efficiency and sharper execution. Unlike earlier funding cycles where valuations expanded rapidly, investors are now negotiating terms aligned with revenue milestones and profitability timelines.

The healthy deal count also suggests that India’s startup pipeline remains active. Incubators, angel networks and micro venture funds are contributing to the ecosystem by bridging funding gaps at the pre Series A stage.

Sector Leaders in Weekly Funding Snapshot

Fintech continued to attract investor interest this week. Digital lending platforms, payment infrastructure providers and wealth management startups are benefiting from rising financial inclusion and digital adoption. India’s expanding digital payments ecosystem creates strong demand for credit assessment, compliance and data analytics solutions.

Software as a service companies also featured prominently in the weekly funding snapshot. Indian SaaS firms with global customer bases are appealing due to recurring revenue models and dollar denominated income streams. Enterprise automation, cybersecurity and data management platforms remain active segments.

Consumer focused startups in ecommerce, health and wellness and food brands secured funding as well. Investors are selectively backing companies with differentiated products and clear distribution strategies, especially those targeting Tier 2 and Tier 3 markets.

Moderate Ticket Sizes Reflect Funding Discipline

The total $200 million raised across 31 deals translates into moderate average ticket sizes. This indicates the absence of mega funding rounds that previously dominated headlines. Instead, capital is being distributed across a larger number of smaller transactions.

This approach reduces systemic risk within the startup ecosystem. Concentration of funding in a few unicorn scale rounds can distort valuations. A diversified funding landscape promotes resilience and encourages competition.

Growth stage startups that raised capital this week likely demonstrated improved unit economics and cost control. Investors have become more cautious about cash burn rates and customer acquisition costs. Sustainable growth metrics are now central to investment decisions.

Regional and Tier 2 Expansion

An important dimension of the weekly funding snapshot is geographic diversification. Several startups raising capital operate beyond traditional metro hubs. Cities such as Jaipur, Ahmedabad, Kochi and Indore have seen increased entrepreneurial activity in recent years.

Lower operating costs and rising digital penetration make these regions attractive for new ventures. Investors are recognizing that scalable businesses can emerge outside established technology clusters.

This regional diversification aligns with broader economic trends. As internet access and logistics infrastructure improve nationwide, startups can serve customers across states without heavy physical presence.

Implications for 2026 Funding Outlook

The weekly funding snapshot provides insight into broader 2026 funding trends. Total capital raised may not match the record levels of 2021, but the ecosystem appears more stable. Investors are focusing on governance, compliance and capital efficiency.

Private equity funds are also monitoring late stage startups for structured growth rounds rather than speculative valuations. This shift could lead to fewer but stronger companies achieving scale.

For founders, the message is clear. Building sustainable revenue streams, maintaining cost discipline and demonstrating product market fit are essential. The era of growth at any cost has been replaced by accountability and financial prudence.

Investor confidence remains intact, but it is increasingly selective. The consistent flow of deals suggests that India continues to be viewed as a long term innovation market with strong domestic demand and export potential in technology services.

The $200 million raised across 31 deals represents more than just weekly capital inflow. It reflects an ecosystem adapting to global capital cycles while maintaining entrepreneurial momentum.

Takeaways

• 31 deals indicate sustained early stage activity in India

• Fintech and SaaS remain leading sectors for investment

• Moderate ticket sizes signal valuation discipline

• Regional startups beyond metros are gaining investor attention

FAQs

Q1. What does the weekly funding snapshot indicate about the startup ecosystem?

It shows steady investor participation across multiple deals, with emphasis on sustainable growth rather than speculative mega rounds.

Q2. Which sectors attracted the most funding this week?

Fintech, SaaS and selective consumer brands were among the most active sectors.

Q3. Are large funding rounds declining?

Mega rounds are less frequent compared to peak years, with investors preferring moderate and diversified allocations.

Q4. How does this trend impact founders?

Founders must focus on profitability, efficient capital use and strong governance to secure funding in the current environment.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Leave a comment