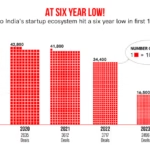

The latest funding roundup from January 13 to 15 highlights diversified capital flows across Indian startups, from gaming and beauty tech to enterprise software and climate focused ventures. The activity signals selective optimism returning to early and growth stage funding despite cautious investor sentiment.

The latest funding roundup for January 13 to 15 reflects a clear shift in how capital is being deployed across the Indian startup ecosystem. Instead of large concentration bets, investors spread capital across multiple sectors, stages, and business models. Gaming platforms, beauty tech brands, SaaS companies, and niche consumer startups all featured in recent funding disclosures, indicating a balanced but cautious revival in deal activity.

Gaming Startups Attract Strategic Capital

Gaming startups emerged as notable beneficiaries during this funding window. Rather than speculative user growth plays, investors backed companies with clear monetisation models such as in app purchases, esports partnerships, and regional language content. The focus was on platforms with strong engagement metrics and defensible communities.

Real money gaming remained selective, with capital flowing only to compliant platforms that demonstrated regulatory preparedness and sustainable unit economics. Casual and mobile gaming startups saw interest from strategic investors aiming to tap India’s growing smartphone user base. The sector’s ability to generate recurring revenue made it attractive despite broader funding moderation.

Beauty Tech and Consumer Brands Gain Momentum

Beauty tech startups continued to attract funding, reinforcing confidence in India’s premium and mass beauty consumption story. Capital flowed into brands leveraging direct to consumer distribution, influencer driven discovery, and efficient supply chains. Investors showed preference for companies with repeat purchase behaviour and strong gross margins.

This round of funding indicated a move away from heavy discount led growth. Beauty tech founders are now focusing on brand equity, offline expansion, and profitability timelines. Tier 2 and Tier 3 demand played a role, as affordable premium products gained traction beyond metros. This made beauty tech one of the more resilient consumer segments during the period.

SaaS and Enterprise Tech See Steady Support

Enterprise focused startups, particularly in SaaS and workflow automation, secured steady funding between January 13 and 15. These deals were largely early to mid stage and centred on companies with overseas client bases or strong domestic enterprise adoption.

Investors prioritised predictable revenue, high retention rates, and lean operating structures. Unlike earlier years, valuations were conservative and tied closely to annual recurring revenue metrics. This approach reflects a broader recalibration where efficiency and capital discipline outweigh aggressive expansion narratives.

Fintech Funding Remains Highly Selective

Fintech startups featured less prominently in this funding roundup compared to previous cycles. Capital flowed primarily to infrastructure led fintechs such as payments enablement, compliance tools, and lending technology platforms rather than consumer facing apps.

Investors remained cautious due to regulatory complexity and longer profitability timelines. Startups with diversified revenue streams and strong partnerships were more likely to close rounds. This selective approach suggests fintech funding is stabilising but far from returning to its peak pace.

Climate and Deeptech Continue to Build Slowly

Climate focused startups and deeptech ventures saw limited but meaningful funding activity. These deals were typically smaller in size and backed by long term investors. Areas such as clean mobility, energy efficiency, and industrial automation attracted interest.

While not headline grabbing, these investments indicate growing confidence in long gestation sectors. Investors appear willing to support innovation where commercialisation pathways are clear, even if timelines are extended. This steady capital flow points to a maturing approach to impact driven investments.

Early Stage Deals Dominate the Funding Mix

A key pattern from the January 13 to 15 funding roundup is the dominance of early stage deals. Seed and Series A rounds outnumbered late stage raises. This suggests investors are more comfortable backing new ideas at reasonable entry points than supporting expensive growth rounds.

Founders raising capital during this period benefited from clear articulation of unit economics and realistic growth plans. Large cheques were rare, but deal closures remained steady. This environment rewards operational clarity over aggressive projections.

What This Funding Pattern Indicates About 2026

The diversified flows seen in this funding window indicate that Indian venture capital is entering a more measured phase. Capital is available, but it is disciplined. Investors are spreading risk across sectors and stages rather than concentrating bets.

Gaming, beauty tech, and enterprise software currently sit at the intersection of demand visibility and manageable costs. Fintech and consumer internet remain under watch. The emphasis on early stage funding suggests confidence in India’s long term startup pipeline, even as near term exits remain limited.

For founders, this environment demands sharper storytelling and execution focus. For investors, it offers opportunities to enter quality businesses at rational valuations. The January 13 to 15 funding activity sets the tone for a year defined by selectivity rather than exuberance.

Takeaways

- Funding from January 13 to 15 was spread across gaming, beauty tech, SaaS, and climate startups

- Early stage deals dominated as investors avoided large valuation risks

- Consumer brands with strong unit economics attracted consistent interest

- Capital deployment reflects discipline, not a slowdown in innovation

FAQs

Why are gaming and beauty tech attracting funding now?

Both sectors show clear monetisation paths and resilient consumer demand.

Is fintech funding declining sharply?

Fintech funding is selective, with focus on infrastructure and compliant models.

Are late stage funding rounds disappearing?

They are fewer, as investors prioritise capital efficiency over scale at any cost.

What does this mean for startup founders in 2026?

Founders need realistic growth plans, strong fundamentals, and clear paths to profitability.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Leave a comment