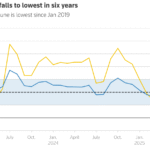

Gold loan demand in India has surged again in 2026, raising questions about whether this reflects financial stress or a strategic liquidity move. The trend is visible across banks and NBFCs, especially in Tier-2 and Tier-3 markets where gold remains a primary financial asset.

Gold Loan Demand Surge Across Banks and NBFCs

Gold loan demand surge has become one of the most notable credit trends in recent quarters. Lenders such as public sector banks and large NBFCs have reported strong growth in gold-backed lending portfolios, driven by rising credit needs and stable gold prices.

Gold loans are attractive because they offer quick disbursal, minimal documentation, and lower interest rates compared to unsecured loans. This makes them a preferred option for borrowers who need immediate liquidity without long approval cycles.

The surge is also supported by relatively high gold prices, which increase the loan value that borrowers can access against the same quantity of gold. This has expanded the appeal of gold loans across income segments.

Is Rising Demand a Sign of Financial Stress

One interpretation of the gold loan demand surge is that it signals underlying financial stress. When households and small businesses face cash flow pressures, they often turn to gold as a last-resort asset to secure funds.

In rural and semi-urban India, gold is widely held as a store of value. During periods of high inflation or rising borrowing costs, monetizing gold becomes a practical option. This trend is particularly visible among MSMEs and self-employed individuals who may not have easy access to formal unsecured credit.

The increase in gold loan uptake can also be linked to higher EMIs on existing loans. As repayment burdens rise, borrowers may use gold loans to manage short-term liquidity gaps.

However, it is important to note that asset-backed borrowing does not always indicate distress. In many cases, it reflects a rational financial decision.

Gold Loans as a Smart Liquidity Strategy

From another perspective, gold loans represent a smart liquidity play. Compared to personal loans or credit cards, gold loans typically come with lower interest rates due to the secured nature of the lending.

Borrowers are increasingly using gold loans as a short-term financing tool rather than a distress mechanism. For example, small traders may use gold-backed credit to fund inventory purchases during peak seasons and repay once cash flows improve.

This behavior is more common in Tier-2 and Tier-3 markets, where access to formal credit has improved but remains uneven. Gold loans bridge this gap by offering a reliable and familiar financing option.

Additionally, the flexibility in repayment structures allows borrowers to manage cash flows more efficiently. Many lenders offer bullet repayment options, where interest is paid periodically and principal is repaid at the end of the tenure.

Role of NBFCs and Digital Gold Lending Trends

NBFC gold loan growth has outpaced traditional bank lending in this segment due to faster processing and wider reach. Companies specializing in gold loans have expanded aggressively in smaller towns, leveraging branch networks and local expertise.

Digital lending is also beginning to influence this segment. Some lenders now offer doorstep gold loan services or digital renewal options, improving convenience for borrowers.

At the same time, regulatory oversight remains strong. The Reserve Bank of India has set guidelines on loan-to-value ratios and risk management to ensure that gold loan growth remains sustainable.

Banks are also increasing their focus on gold loans as a low-risk asset class, especially in a moderately tight liquidity environment. This dual participation from banks and NBFCs is accelerating overall market growth.

What This Trend Means for the Economy

The gold loan demand surge reflects a broader shift in how Indian households and businesses manage liquidity. It highlights the continued importance of physical assets in the financial ecosystem, even as digital credit expands.

For the economy, this trend has both positive and cautionary aspects. On the positive side, it ensures that credit flow continues even when unsecured lending slows down. This supports consumption and small business activity.

On the risk side, a sharp increase in gold-backed borrowing could indicate pressure in certain segments, particularly if borrowers struggle to repay and are forced to liquidate assets.

The key takeaway is that gold loans are serving as both a safety net and a strategic tool, depending on the borrower’s financial situation.

Takeaways

- Gold loan demand is rising due to both liquidity needs and strategic borrowing

- Higher gold prices are increasing borrowing capacity for households

- NBFCs are driving growth in Tier-2 and Tier-3 markets with faster access to credit

- The trend reflects both financial resilience and underlying stress in segments

FAQs

Why are gold loans becoming popular again in India?

Gold loans offer quick access to funds, lower interest rates, and minimal documentation, making them attractive during periods of high borrowing costs.

Does rising gold loan demand indicate financial stress?

It can indicate stress in some cases, but it is also used as a smart liquidity tool by borrowers managing short-term needs.

How do gold loans compare to personal loans?

Gold loans generally have lower interest rates because they are secured, while personal loans are unsecured and more expensive.

Are gold loans safe for borrowers?

They are relatively safe if repaid on time, but failure to repay can lead to the loss of pledged gold.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Leave a comment