India’s UPI growth vs profitability debate has intensified in 2026 as transaction volumes hit record highs while revenue models remain limited. The core question is whether the current zero MDR framework can support long-term sustainability for banks, fintechs, and payment providers.

UPI Growth Trajectory and Market Expansion

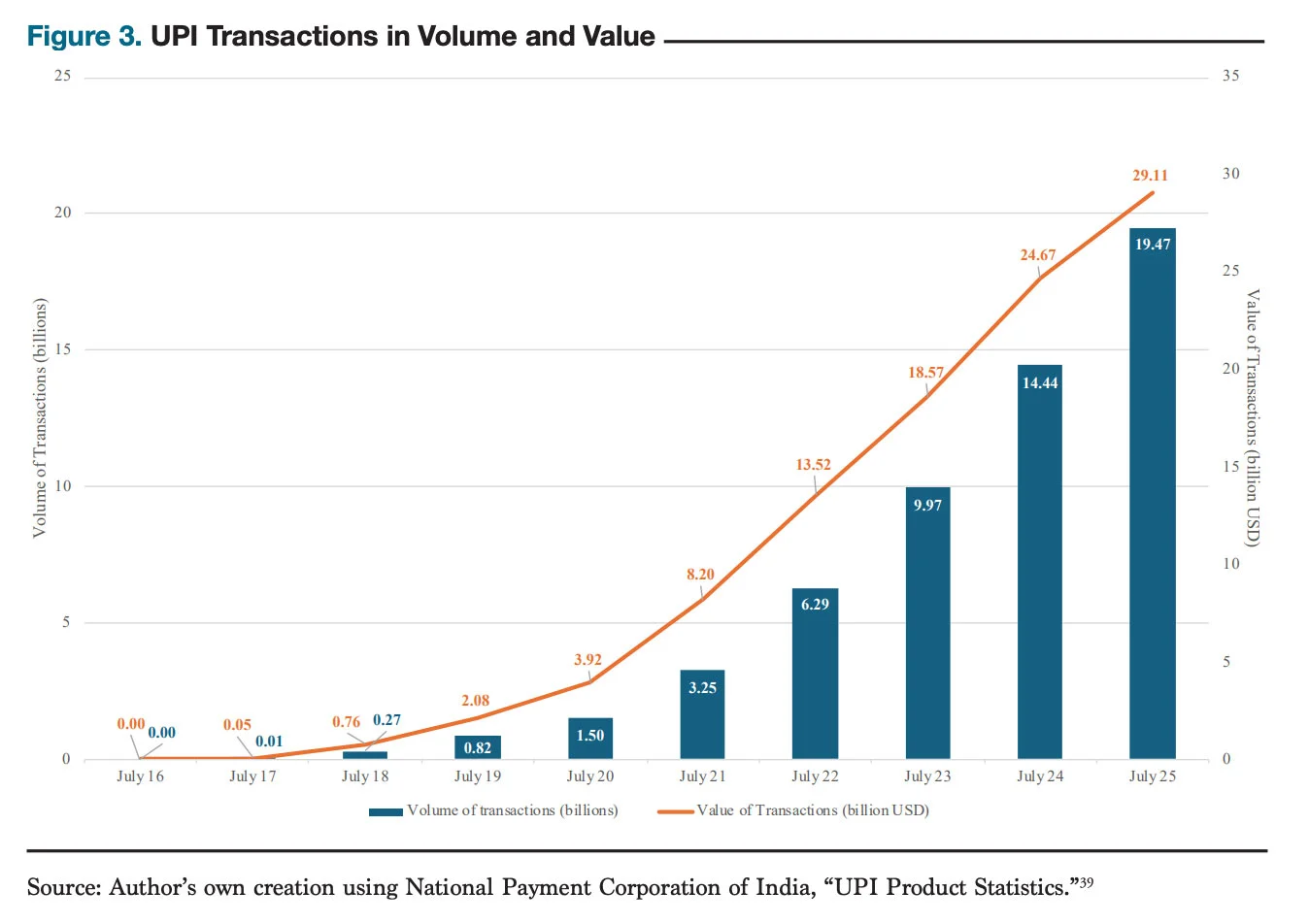

UPI growth vs profitability is now a central issue in India’s digital payments ecosystem. Unified Payments Interface has scaled rapidly, crossing billions of monthly transactions and becoming the default payment method across urban and rural markets.

Adoption has been particularly strong in Tier-2 and Tier-3 cities, where UPI has replaced cash for small-value transactions. Street vendors, small retailers, and service providers now rely heavily on QR-based payments, reducing dependency on physical currency.

The government and the National Payments Corporation of India have actively supported this expansion by maintaining zero merchant discount rate for UPI transactions. This has ensured widespread adoption but has also limited direct revenue generation for ecosystem players.

As usage continues to grow, the gap between scale and monetization is becoming more visible.

Zero MDR Policy and Revenue Constraints

Zero MDR UPI policy remains the biggest constraint on profitability. Unlike credit cards and some debit card transactions, UPI payments do not generate transaction fees for banks or payment service providers in most cases.

This means that while transaction volumes are increasing, revenue per transaction remains negligible. Banks incur infrastructure and operational costs without proportional income, while fintech companies depend on indirect monetization strategies.

The government has introduced incentive schemes to compensate stakeholders for processing UPI transactions, but these incentives are limited and not guaranteed long term. This creates uncertainty around sustainable revenue models.

For payment apps, customer acquisition and retention costs continue to rise, further adding pressure on profitability.

Fintech Monetization Strategies Around UPI

UPI monetization India is evolving through alternative revenue streams rather than direct transaction fees. Fintech companies are leveraging UPI as an entry point to offer additional financial services.

These include credit products such as buy now pay later, personal loans, and credit lines linked to UPI transactions. By analyzing transaction data, fintechs can assess user behavior and extend credit to eligible customers.

Other monetization avenues include wealth management, insurance distribution, and merchant services such as inventory tools and analytics. These value-added services generate revenue while keeping core payments free.

Large players are also exploring subscription models for merchants, offering premium features beyond basic payment acceptance. However, adoption of such paid services is still limited, especially in price-sensitive markets.

Cost Pressures on Banks and Payment Ecosystem

Banks play a critical role in the UPI ecosystem as they handle transaction settlement and infrastructure. However, rising transaction volumes are increasing operational costs without a matching increase in revenue.

Payment service providers and third-party apps also invest heavily in technology, cybersecurity, and compliance. These costs are necessary to maintain reliability and trust in the system.

In a high-volume, low-margin environment, efficiency becomes crucial. Players with strong balance sheets and diversified revenue streams are better positioned to sustain operations.

Smaller fintech firms, on the other hand, may face challenges in achieving profitability if they rely solely on payments without expanding into adjacent services.

Sustainability Outlook for UPI at Scale

The sustainability of UPI depends on balancing financial inclusion goals with economic viability. The current model has successfully driven adoption, but long-term sustainability may require policy adjustments or new revenue mechanisms.

One possibility is the introduction of a nominal MDR for large merchants while keeping small transactions free. Another approach is expanding government incentives or encouraging innovation in value-added services.

Globally, most digital payment systems rely on some form of transaction fee. India’s zero MDR approach is unique and has been effective in scaling adoption, but it may need refinement as the ecosystem matures.

Despite profitability concerns, UPI remains a critical infrastructure for India’s digital economy. Its role in driving financial inclusion, reducing cash usage, and enabling seamless transactions is unlikely to diminish.

Takeaways

- UPI has achieved massive scale but faces structural profitability challenges

- Zero MDR policy limits direct revenue for banks and fintech players

- Fintechs are focusing on credit and value-added services for monetization

- Sustainability may require policy adjustments or new business models

FAQs

Why is UPI not profitable despite high usage?

UPI transactions typically do not generate fees due to the zero MDR policy, limiting direct revenue for ecosystem participants.

How are fintech companies making money from UPI?

They use UPI as a gateway to offer credit, insurance, and other financial services that generate revenue.

Will UPI start charging users or merchants?

There is no immediate change, but discussions around selective fees or alternative models continue.

Is UPI sustainable in the long run?

It is sustainable with evolving monetization strategies and potential policy adjustments to balance growth and profitability.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Leave a comment