India’s retail inflation trend is directly influencing EMI costs for borrowers in Tier-2 cities. As inflation pressures remain uneven, lending rates and household repayment capacity are being reshaped, especially for middle-income families dependent on loans for housing, vehicles, and consumption.

Retail Inflation Trends in India and Policy Response

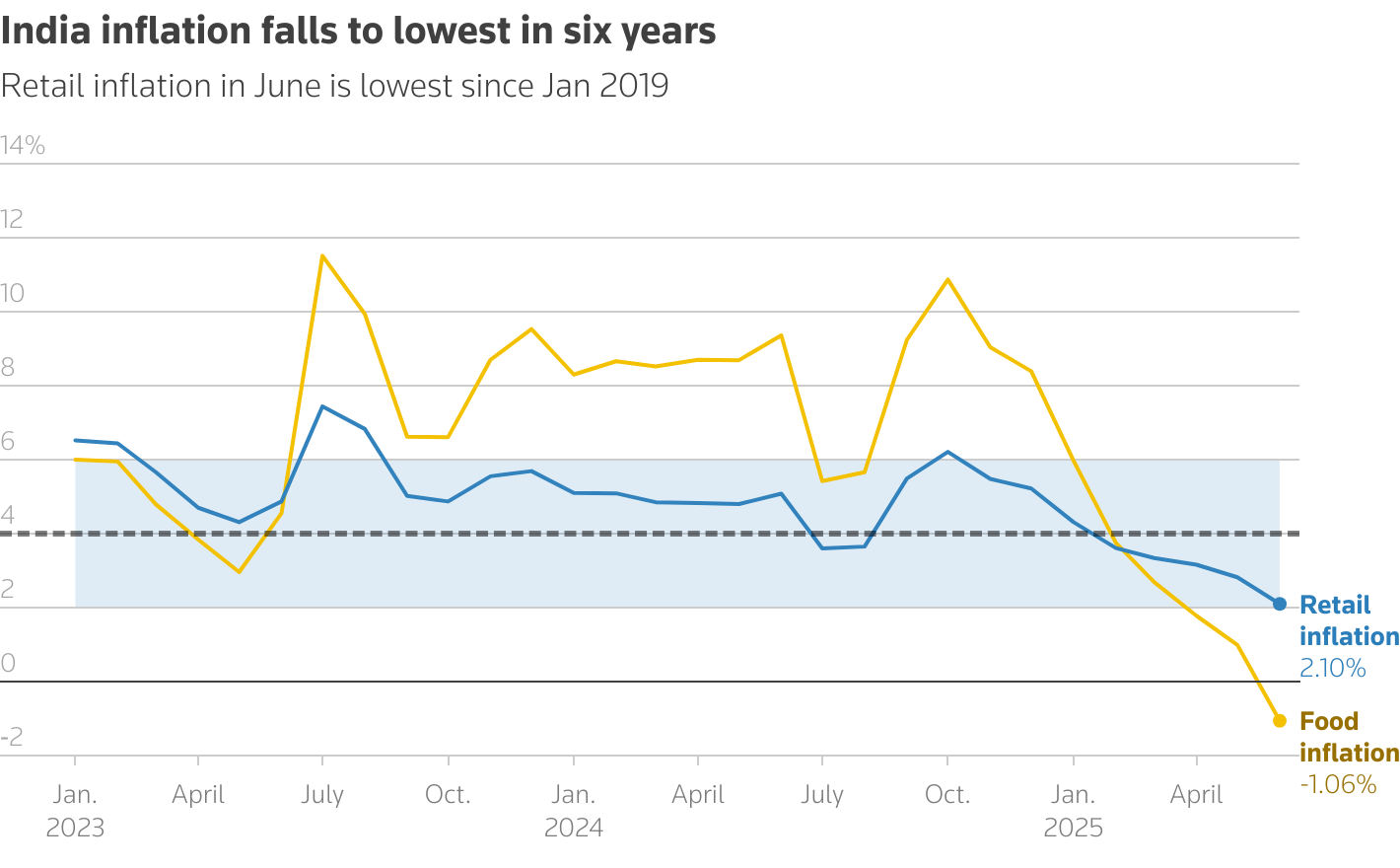

India retail inflation trend has remained within the Reserve Bank of India’s tolerance band of 2 to 6 percent in recent quarters, but volatility in food prices continues to create periodic spikes. Inflation is primarily measured through the Consumer Price Index, with food and fuel contributing significantly to fluctuations.

When inflation rises, the RBI typically responds by tightening monetary conditions or maintaining higher interest rates for longer periods. This directly impacts repo-linked lending rates, which most modern retail loans are tied to. As a result, even small changes in policy rates can translate into noticeable changes in EMIs.

For borrowers in Tier-2 cities, where income growth is steady but not rapid, these changes can significantly alter monthly financial planning. Unlike metro borrowers, many households operate with tighter financial buffers, making them more sensitive to inflation-driven rate changes.

EMI Burden Impact on Tier-2 Households

EMI burden in Tier-2 cities has increased gradually over the past two years due to cumulative rate hikes and delayed rate cuts. Home loans, which are typically long-term and floating rate, are the most affected.

For example, a one percentage point increase in lending rates can raise monthly EMIs by several thousand rupees depending on loan size. In cities like Nagpur, Jaipur, and Indore, where property purchases are often financed through high loan-to-value ratios, this creates immediate pressure on household budgets.

Auto loans and personal loans are also becoming costlier. While the absolute ticket size is smaller than home loans, the shorter tenure means borrowers feel the impact faster. This is leading to cautious spending behavior, especially among salaried individuals and small business owners.

Another emerging trend is the extension of loan tenures by lenders to keep EMIs stable. While this reduces short-term burden, it increases the total interest paid over the life of the loan.

Banking and NBFC Lending Trends Under Inflation Pressure

Retail lending trends India show that banks and NBFCs are recalibrating their strategies in response to inflation and interest rate dynamics. Lenders are becoming more selective in underwriting, focusing on borrowers with stable income profiles and lower default risk.

NBFCs, which serve a large share of Tier-2 and Tier-3 borrowers, are facing slightly higher cost of funds. This is because their borrowing rates are linked to market conditions, which remain influenced by inflation expectations. As a result, lending rates for end consumers have edged higher.

At the same time, co-lending models between banks and NBFCs are helping maintain credit flow. These partnerships allow risk sharing and enable lenders to continue serving borrowers in smaller cities without significantly increasing exposure.

Digital lending platforms are also playing a role by offering faster approvals and customized repayment structures. However, interest rates on such platforms can vary widely depending on borrower risk profiles.

Consumption Patterns and Financial Behavior Shift

Rising EMI obligations are beginning to influence consumption patterns in Tier-2 markets. Households are prioritizing essential spending and delaying discretionary purchases such as electronics, travel, and lifestyle upgrades.

This shift is particularly visible among first-time borrowers who entered the credit system during the low interest rate period of 2020 to 2022. As rates adjusted upward, their repayment burden increased without a corresponding rise in income.

Savings behavior is also changing. More households are building emergency funds to manage potential EMI shocks, while some are prepaying loans when possible to reduce long-term interest costs.

For small business owners, higher EMIs on business loans or personal borrowings can affect cash flow, limiting their ability to reinvest in growth.

Outlook for Inflation and Borrowers in 2026

The outlook for inflation remains dependent on food prices, global commodity trends, and domestic demand conditions. While the RBI aims to keep inflation within its target range, short-term fluctuations are likely to continue.

For borrowers, this means interest rates may not decline sharply in the near term. Stability rather than aggressive easing is the more likely scenario. This keeps EMI burdens elevated but predictable.

Tier-2 cities will remain a key focus area for lenders due to growing demand, but credit growth may become more measured. Borrowers will need to plan finances carefully, factoring in potential rate changes and maintaining adequate liquidity buffers.

Takeaways

- Retail inflation directly impacts EMI costs through interest rate movements

- Tier-2 households are more sensitive to EMI increases due to tighter income buffers

- Banks and NBFCs are becoming more selective in lending under inflation pressure

- Borrowers are adjusting spending and savings habits to manage higher EMIs

FAQs

How does inflation affect EMIs in India?

Higher inflation often leads to higher interest rates, which increases EMIs on floating rate loans such as home and auto loans.

Why are Tier-2 cities more affected by EMI changes?

Income levels and savings buffers are typically lower than metros, making households more sensitive to rising monthly obligations.

Are interest rates expected to fall soon?

Rates may stabilize, but sharp cuts are unlikely unless inflation declines significantly and consistently.

What can borrowers do to manage higher EMIs?

Options include partial prepayment, refinancing loans, extending tenure, or building emergency savings to handle fluctuations.

(Primary keyword: India retail inflation trend EMI impact, Secondary keywords: EMI burden Tier-2 cities, RBI inflation impact loans, retail lending India trends, home loan interest rates India, NBFC lending rates)

India Retail Inflation Trend and EMI Burden in Tier-2 Cities

India’s retail inflation trend is shaping borrowing costs across the country, with a visible impact on EMI burden in Tier-2 cities. As inflation remains within a controlled but elevated range, households are adjusting to higher loan repayments and tighter monthly budgets.

Retail Inflation Trend and Interest Rate Transmission

India retail inflation trend has stayed largely within the Reserve Bank of India’s target band of 2 to 6 percent, but persistent food inflation continues to create pressure points. The central bank uses repo rate adjustments and liquidity management to control inflation, which directly influences lending rates across banks and NBFCs.

Most retail loans today are linked to external benchmarks like the repo rate. This means any change in monetary policy is transmitted relatively quickly to borrowers. Over the past two years, cumulative rate increases have pushed lending rates higher, even though inflation has shown signs of moderation.

For borrowers in Tier-2 cities, this transmission is more visible because loan affordability is closely tied to monthly income. Even marginal increases in rates can disrupt repayment planning, especially for households with multiple loans.

EMI Burden Rising in Tier-2 Housing Markets

EMI burden Tier-2 cities has increased steadily, particularly in the housing segment. Home loans form the largest share of retail credit, and their long tenure makes them highly sensitive to interest rate cycles.

In cities such as Nagpur, Bhopal, and Kochi, property demand has remained strong, but higher EMIs are beginning to impact affordability. Borrowers who took loans during the low-rate period have seen their EMIs rise or loan tenures extend significantly.

Banks often adjust tenures instead of increasing EMIs immediately, which helps borrowers manage monthly cash flow. However, this leads to higher overall interest payouts over time. For middle-income households, this trade-off is becoming a key financial decision.

The effect is not limited to new borrowers. Existing borrowers with floating rate loans are also experiencing changes in repayment schedules, adding pressure to long-term financial planning.

Auto Loans and Personal Credit Feeling the Pressure

Beyond housing, auto loans and personal loans are also reflecting the impact of inflation-linked interest rates. While these loans have shorter tenures, the higher interest rates are quickly visible in monthly installments.

Retail lending India trends indicate that borrowers are becoming more cautious about taking on new debt. Vehicle purchases in smaller cities are increasingly being delayed or financed with higher down payments to reduce EMI exposure.

Personal loans, often used for consumption or emergencies, are seeing stricter underwriting standards. Lenders are focusing on credit scores and income stability, especially in a high-rate environment.

NBFCs, which cater significantly to Tier-2 markets, are passing on increased funding costs to borrowers. This has made credit slightly more expensive compared to previous years.

Changing Consumption Patterns in Non-Metro India

The rise in EMI burden is influencing spending behavior across Tier-2 cities. Households are prioritizing essential expenses such as housing, education, and healthcare while cutting back on discretionary spending.

This shift is affecting sectors like consumer durables, travel, and lifestyle products, which rely heavily on financed purchases. Businesses operating in these segments are witnessing more cautious demand from smaller cities.

At the same time, financial awareness is improving. Borrowers are actively exploring options such as loan prepayment, refinancing, and balance transfers to manage interest costs.

Small business owners are also adapting by optimizing cash flows and limiting leverage. Higher EMIs on business-related loans can directly affect profitability, especially in sectors with thin margins.

Outlook for Inflation and Borrowers in 2026

The outlook for India retail inflation trend remains dependent on food supply conditions, global commodity prices, and domestic demand. While inflation is expected to stay within the RBI’s tolerance range, sharp declines are unlikely in the near term.

This suggests that interest rates may remain stable rather than decline significantly. For borrowers, this means EMIs will stay elevated but predictable, allowing for better financial planning.

Tier-2 cities will continue to drive credit growth due to rising aspirations and economic activity. However, both lenders and borrowers are expected to adopt a more cautious approach, balancing growth with financial stability.

Takeaways

- Retail inflation continues to influence EMI costs through interest rate transmission

- Tier-2 households are facing higher repayment pressure, especially on home loans

- NBFCs and banks are tightening lending standards in a high-rate environment

- Consumers are adjusting spending habits and prioritizing financial stability

FAQs

How does retail inflation affect EMIs in India?

Retail inflation influences interest rates set by the RBI, which directly impacts EMIs on floating rate loans.

Why are Tier-2 cities more sensitive to EMI changes?

Income levels and savings buffers are relatively lower, making households more vulnerable to rising loan costs.

Are borrowers seeing higher EMIs or longer tenures?

Both are happening. Banks often extend loan tenures to keep EMIs manageable, increasing total interest paid.

What strategies can help manage higher EMI burden?

Borrowers can consider partial prepayment, refinancing, or increasing down payments to reduce overall loan cost.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Leave a comment