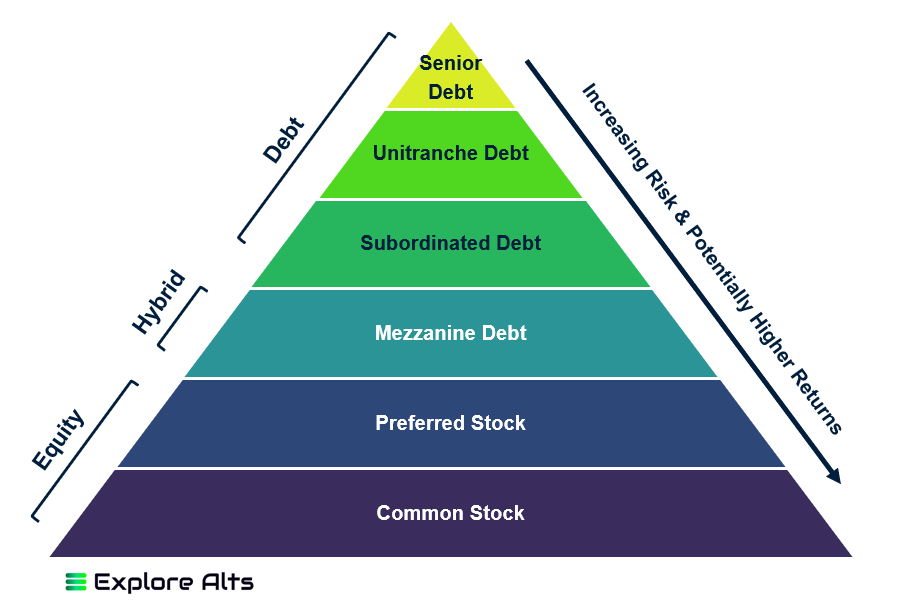

Private credit yields of up to 22 percent are changing startup financing calculus across India as founders reassess capital choices in a tighter funding environment. High yield debt is emerging as a serious alternative to equity, altering risk, growth planning, and control dynamics for startups.

Private credit yields have moved from the margins of startup finance into mainstream conversations. With venture capital more selective and equity rounds harder to close, startups are increasingly evaluating private credit as a funding option. Yields reaching up to 22 percent reflect the higher risk lenders perceive in early and growth stage ventures. At the same time, they signal how urgently founders are seeking non dilutive capital to extend runway and protect ownership.

What is driving the rise in private credit yields

The sharp rise in private credit yields is primarily driven by risk repricing. Lenders are factoring in higher default probabilities, slower exits, and uncertain revenue visibility. Unlike banks, private credit funds are not constrained by traditional lending norms, allowing them to price risk aggressively. Startups seeking capital outside equity rounds often lack collateral or consistent cash flows, pushing yields higher. In addition, global interest rate conditions have lifted baseline return expectations. Private credit funds must now offer returns that justify illiquidity and startup risk, leading to double digit yields that can touch 22 percent in certain structures.

Why startups are still choosing high cost credit

Despite the high cost, startups are opting for private credit for strategic reasons. Equity dilution has become more expensive in a valuation conscious market. Founders who raised capital at peak valuations are reluctant to accept down rounds that reset ownership and control. Private credit allows them to raise funds without immediately impacting equity stakes. For revenue generating startups with predictable cash flows, debt can bridge short term needs such as working capital, expansion, or regulatory costs. The financing calculus now weighs dilution risk against interest burden, a trade off many founders are willing to make.

How private credit changes growth planning

Private credit imposes discipline that equity often does not. High interest obligations force startups to prioritise cash flow management and realistic growth plans. Burn heavy expansion strategies become harder to justify when monthly repayments are due. As a result, startups using private credit tend to focus on core revenue streams, cost optimisation, and faster breakeven paths. This shift is altering how founders plan milestones. Instead of chasing scale at any cost, the emphasis moves to unit economics and operational efficiency. In this sense, private credit is reshaping behaviour, not just balance sheets.

Impact on early stage versus growth stage startups

The impact of high yield private credit differs by stage. Early stage startups generally find such debt unsuitable due to lack of stable revenues. For them, equity remains the primary option despite tougher terms. Growth stage startups, particularly in SaaS, fintech infrastructure, and B2B services, are better positioned to absorb high yield debt. These companies often have recurring revenues that can support repayments. Private credit thus widens the gap between early and later stage funding strategies. It rewards startups that reach revenue stability faster and penalises those that remain dependent on external capital.

Investor perspective on private credit opportunities

From the investor side, private credit yields of up to 22 percent are attractive in a low liquidity environment. Returns are contractually defined rather than dependent on uncertain exits. This appeals to investors seeking predictable income rather than long term capital gains. However, the risk remains high. Startup defaults can erode returns quickly, making due diligence critical. Investors are focusing on covenant structures, revenue visibility, and founder credibility. The rise of private credit reflects a broader shift toward downside protection in startup investing.

Risks startups must account for

High yield private credit is not without risks. Interest burdens can strain cash flows, especially if growth slows or receivables are delayed. Some debt structures include strict covenants that limit operational flexibility. Failure to meet repayment schedules can trigger penalties or forced restructuring. Startups that overestimate their ability to service debt may find themselves worse off than if they had accepted equity dilution. The financing calculus must therefore consider downside scenarios, not just immediate capital needs.

How this trend is reshaping the startup ecosystem

The growing role of private credit is reshaping the startup ecosystem by introducing more financial realism. Capital is no longer uniformly patient. Founders must justify funding choices with clearer paths to sustainability. Venture investors also adapt by encouraging portfolio companies to use debt strategically rather than raising frequent equity rounds. Over time, this could lead to fewer but stronger startups that grow within their means. It may also reduce speculative funding cycles that inflate valuations without supporting fundamentals.

What founders should consider before opting for private credit

Founders evaluating private credit must assess revenue predictability, cash flow resilience, and growth timelines. High yields demand disciplined execution. Debt should fund revenue generating activities rather than experimental expansion. Transparency with stakeholders and realistic forecasting are essential. Private credit can be a powerful tool when used deliberately, but it magnifies mistakes when used as a substitute for viable business models.

Takeaways

- Private credit yields up to 22 percent reflect higher risk and tighter capital markets.

- Startups are choosing debt to avoid dilution despite higher financing costs.

- High yield credit enforces financial discipline and cash flow focus.

- Misuse of private credit can amplify downside risks for founders.

FAQs

Why are private credit yields so high for startups?

They reflect elevated risk, illiquidity, and uncertainty around startup cash flows and exits.

Is private credit replacing venture capital?

No. It complements equity funding but is mainly suitable for revenue generating startups.

Which startups benefit most from private credit?

Growth stage startups with predictable revenues and strong unit economics benefit the most.

What is the biggest risk of using high yield private credit?

Cash flow strain and restrictive covenants can limit flexibility and increase default risk.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Leave a comment