Venture capital sentiment heading into 2026 reflects cautious optimism tempered by deal flow reality. Investors express confidence in long-term fundamentals, yet deployment remains selective as valuation discipline, exit uncertainty, and portfolio consolidation continue to shape how capital actually moves.

Venture capital sentiment heading into 2026 sits at an inflection point. This topic is informational with a forward-looking news context, requiring analysis rather than prediction. While investor conversations suggest renewed confidence, real deal flow tells a more measured story. Capital is available, but it is patient, conditional, and increasingly demanding. Understanding this gap between sentiment and action is critical for founders, funds, and ecosystem operators.

Why Sentiment Has Improved Compared to Previous Years

Investor sentiment entering 2026 is more stable than during peak uncertainty periods. Secondary keywords such as VC confidence trends and investor outlook 2026 apply here. Inflation pressures have eased, interest rate trajectories are clearer, and businesses have adjusted to capital scarcity.

Funds have had time to recalibrate expectations after the sharp corrections of earlier years. Portfolios are cleaner, burn rates are lower, and governance standards have improved. This creates psychological room for optimism. However, sentiment alone does not automatically translate into faster deal execution or larger cheque sizes.

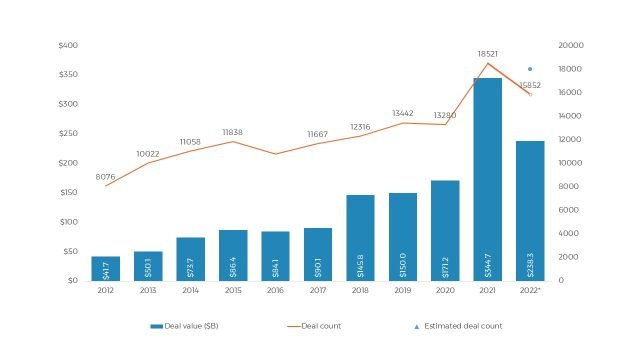

Deal Flow Reality Remains Selective

Despite improved sentiment, deal flow reality remains constrained. Secondary keywords like venture deal flow slowdown and funding selectivity fit here.

Investors are seeing a high volume of pitches but closing fewer deals. Due diligence cycles are longer, and investment committees demand stronger proof points. Many opportunities stall due to valuation mismatches or unclear paths to profitability. As a result, deployment velocity has not matched the optimism expressed in market commentary.

This gap highlights a key shift. Capital is no longer chasing growth narratives. It is waiting for evidence of durable demand, pricing power, and operational discipline.

Valuation Discipline Shapes Investment Decisions

Valuation remains one of the strongest friction points heading into 2026. Secondary keywords such as startup valuation discipline and pricing reset apply here.

Founders anchored to past benchmarks often struggle to close rounds. Investors benchmark against current revenue, margins, and cash flow visibility rather than future scale alone. This results in fewer deals but higher quality alignment when rounds do close.

For venture funds, disciplined entry prices are essential for return protection. This focus reduces downside risk but also slows deal flow, reinforcing the disconnect between positive sentiment and actual capital movement.

Portfolio Management Takes Priority Over New Bets

Another reason deal flow remains muted is portfolio focus. Secondary keywords like VC portfolio consolidation and follow-on funding strategy fit this section.

Many funds prioritise supporting existing portfolio companies that demonstrate execution strength. Follow-on capital absorbs a significant share of available dry powder. This limits capacity for new investments, especially at later stages.

Funds also reassess underperforming assets, delaying exits or write-downs. This internal housekeeping consumes time and attention, even as external sentiment improves.

Sectoral Preferences Drive Capital Concentration

Venture capital sentiment is not uniform across sectors. Secondary keywords such as sectoral VC trends and investment focus areas apply here.

Enterprise software, infrastructure tech, climate solutions, healthcare, and deeptech attract consistent interest. These sectors align with long-term demand and defensibility. Consumer internet and capital-intensive expansion models face higher scrutiny unless differentiation is clear.

This concentration means deal flow exists but only in specific lanes. Founders outside favoured sectors perceive the market as frozen, while those within priority areas continue to raise capital.

Founder Behaviour Adjusts to the New Reality

Founders entering 2026 are more pragmatic. Secondary keywords like founder fundraising strategy and startup readiness apply here.

Many delay fundraising until metrics improve. Others reduce round sizes or extend runway before approaching investors. Pitch narratives focus on sustainability, unit economics, and resilience rather than rapid scale.

This behaviour improves alignment but also reduces the volume of active deals at any given time. Fewer founders are willing to test the market prematurely, contributing to lower visible deal flow despite positive sentiment.

Exit Visibility Still Limits Aggressive Deployment

Exit conditions remain a constraint. Secondary keywords such as venture exits outlook and liquidity constraints fit here.

Public markets have not fully reopened for high-growth tech listings, and M&A activity remains selective. Without clear exit pathways, investors remain cautious about deploying large amounts of capital quickly.

This reinforces the wait-and-watch approach. Sentiment may be optimistic, but capital moves only when liquidity confidence improves.

What This Means for 2026 and Beyond

Venture capital sentiment heading into 2026 suggests stability, not acceleration. Secondary keywords like venture capital outlook India and global VC trends fit here.

The ecosystem is healthier but more deliberate. Capital will flow to businesses that meet higher standards, while speculative models struggle. Over time, this dynamic supports sustainable growth rather than boom-bust cycles.

Optimism is real, but it is disciplined. The gap between sentiment and deal flow will narrow only when valuations, exits, and execution align simultaneously.

Takeaways

- Venture capital sentiment entering 2026 is cautiously optimistic but measured

- Deal flow remains selective due to valuation discipline and portfolio focus

- Sector concentration drives uneven access to capital

- Exit uncertainty continues to limit aggressive deployment

FAQs

Why is there optimism despite slow deal flow

Macro stability and improved startup discipline support confidence, even if capital deployment remains cautious.

Are investors actively looking for new deals

Yes, but only within preferred sectors and with strong fundamentals.

What is the biggest barrier to faster deal flow

Valuation mismatches and limited exit visibility slow investment decisions.

Will deal flow improve in 2026

Gradual improvement is likely, driven by better alignment between founders, investors, and market conditions.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Leave a comment