The question of whether RBI can cut interest rates in 2026 is gaining attention as inflation trends soften and global economic conditions remain uncertain. Any rate change will directly influence loan costs, EMIs, and borrowing demand across India.

RBI Interest Rate Outlook 2026 and Policy Signals

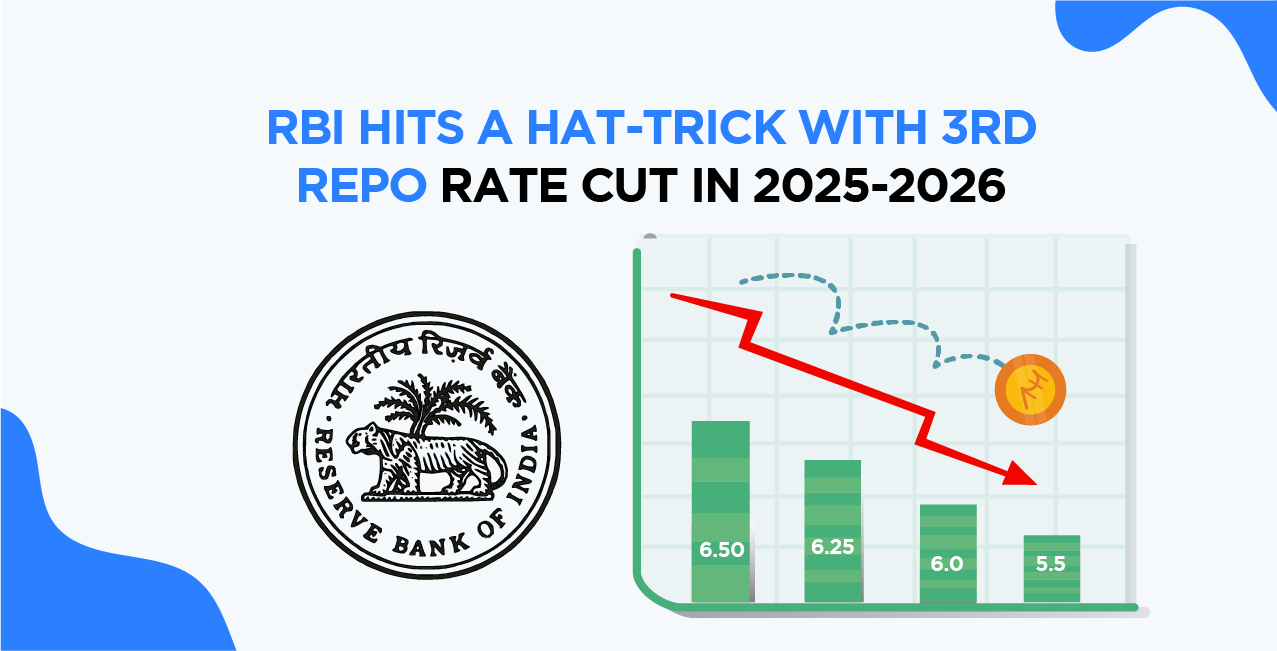

The possibility that RBI may cut interest rates in 2026 depends largely on inflation control and economic growth stability. As of recent monetary policy cycles, the Reserve Bank of India has maintained a cautious stance, prioritizing inflation targeting within its defined range of 4 percent with a tolerance band.

If inflation shows sustained moderation and remains within this target, the central bank may consider a rate cut to support economic growth. However, RBI typically avoids aggressive shifts unless macroeconomic indicators clearly justify easing.

Global signals also matter. Central banks in developed economies have maintained tight monetary policies due to persistent inflation concerns. If global rates remain high, RBI may delay cuts to avoid capital outflows and currency volatility.

How Interest Rate Cuts Affect Loans and EMIs

When RBI reduces the repo rate, it lowers the cost at which banks borrow funds. This generally leads to lower lending rates for consumers, although the transmission may not be immediate or uniform.

For borrowers, a rate cut translates into lower EMIs or shorter loan tenures. Home loans, which are often linked to external benchmark lending rates, tend to reflect changes more quickly compared to older loan structures.

For example, even a 25 basis point reduction can lead to noticeable savings over long tenures. On a typical home loan, this could reduce monthly EMIs or help borrowers repay faster without increasing their monthly outflow.

However, the actual benefit depends on how efficiently banks pass on the rate cuts. In some cases, banks may delay transmission due to liquidity conditions or internal cost structures.

Impact on Retail Borrowers and Tier-2 India

For retail borrowers in Tier-2 and Tier-3 cities, interest rate cuts can significantly improve credit accessibility. Lower EMIs make loans more affordable, encouraging first-time homebuyers, small business owners, and vehicle buyers to enter the credit market.

In cities like Jaipur, Lucknow, and Nagpur, where income levels are growing but remain price-sensitive, even small reductions in borrowing costs can drive demand.

Lower interest rates also improve cash flow for existing borrowers. This can increase disposable income, which in turn supports consumption in local economies.

For MSMEs, cheaper credit reduces financing costs and supports expansion plans. Businesses can invest in inventory, equipment, or hiring without taking on excessive financial stress.

Banking Sector Response and Credit Growth Trends

Banks play a critical role in determining how rate cuts translate into real benefits. In recent years, the shift to external benchmark-linked lending rates has improved transparency and faster transmission for retail loans.

However, banks also consider factors such as deposit rates, liquidity, and credit risk before adjusting lending rates. If deposit costs remain high, the reduction in lending rates may be gradual.

Credit growth trends also influence decision-making. If loan demand is already strong, banks may not aggressively lower rates. On the other hand, weaker credit demand could push lenders to pass on benefits more quickly to attract borrowers.

The balance between maintaining margins and driving credit growth will shape how effectively rate cuts impact borrowers.

Risks and Uncertainties Around Rate Cuts

While rate cuts can stimulate growth, they are not without risks. If inflation resurges due to external shocks such as commodity price spikes or supply disruptions, RBI may be forced to maintain or even increase rates.

Currency stability is another concern. Lower interest rates can lead to capital outflows if global investors find better returns elsewhere. This can put pressure on the rupee.

Additionally, excessive credit growth driven by low rates can lead to asset quality concerns in the banking system. RBI typically takes a measured approach to avoid such imbalances.

Therefore, any rate cut in 2026 is likely to be gradual and data-driven rather than aggressive.

What Borrowers Should Expect in 2026

Borrowers should not assume immediate or sharp reductions in loan costs. Instead, the outlook suggests a gradual easing cycle if inflation remains under control.

For new borrowers, waiting for marginal rate reductions could improve affordability. Existing borrowers should monitor their loan benchmarks and consider refinancing options if significant rate cuts occur.

Financial planning remains important. Even with lower rates, borrowers should assess repayment capacity and avoid over-leveraging.

The broader trend indicates that while rate cuts are possible, they will depend on evolving economic conditions rather than a fixed timeline.

Takeaways

RBI may consider rate cuts in 2026 if inflation remains stable

Lower interest rates can reduce EMIs and improve loan affordability

Tier-2 borrowers and MSMEs stand to benefit from cheaper credit

Rate cuts are likely to be gradual and dependent on global factors

FAQs

Will RBI definitely cut interest rates in 2026?

There is no certainty. The decision depends on inflation trends, economic growth, and global financial conditions.

How much can EMIs reduce if rates are cut?

Even a small reduction of 25 basis points can lower EMIs or shorten loan tenure, depending on the loan size and duration.

Which loans benefit the most from rate cuts?

Home loans and other floating rate loans linked to external benchmarks usually benefit the most.

Should borrowers wait for rate cuts before taking loans?

It depends on individual needs. Waiting may help slightly, but delaying important financial decisions solely for potential rate cuts may not always be practical.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Leave a comment